Inventory market corrections (a decline of 10% or extra from the current excessive) is usually a present to dividend-seeking buyers. As inventory costs fall, dividend yields rise, enabling buyers to lock in larger yields on many prime dividend shares.

I have been capitalizing on the current inventory market correction by shopping for extra shares of a lot of my favourite dividend shares. Amongst these I lately bought have been Blackstone(NYSE: BX), Starbucks(NASDAQ: SBUX), and Verizon(NYSE: VZ). This is whyI feel they’re nice dividend shares to purchase proper now.

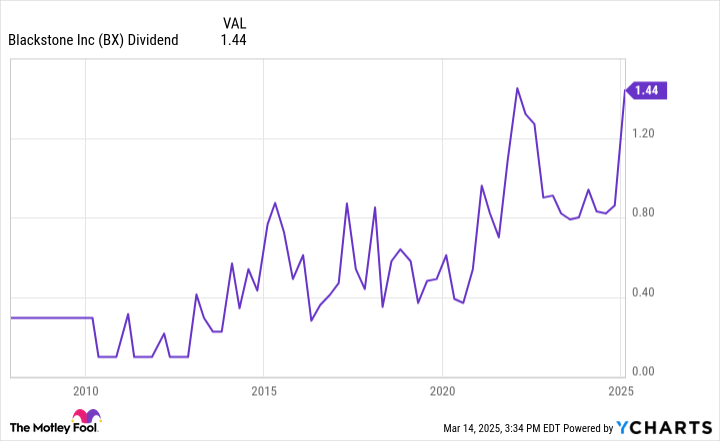

Personal fairness large Blackstone has misplaced almost 30% of its worth from the current peak. That sell-off has pushed its dividend yield as much as 2.8%, greater than double the S&P 500‘s present yield of 1.3%.

Blackstone is not your typical dividend inventory. It does not pay a set quarterly dividend like most corporations. As an alternative, the main various asset supervisor returns the majority of its distributable earnings to buyers every quarter by way of dividends and share repurchases. Because of that dividend coverage, its cost can fluctuate, generally considerably:

Nevertheless, the payout has been on a typically upward trajectory over the previous decade and a half.I anticipate therising pattern will proceed as Blackstone grows its property below administration (AUM), fee-based earnings, and efficiency revenues.

Driving that view is the expectation that buyers will proceed to extend their allocations to various investments like non-public fairness, actual property, and credit score as a result of they have a tendency to generate larger returns with decrease volatility than the general public inventory and bond markets. Based on a forecast by Preqin, the worldwide options market will hit $30 trillion by 2030, up from $17 trillion on the finish of 2023.

That progress ought to profit Blackstone’s main various franchises. With Blackstone’s inventory down sharply amid the market sell-off, I may probably earn a lovely whole return as its value recovers and its dividend rises.

Starbucks inventory has slumped about 15% from its current excessive, which has pushed the espresso large’s dividend yield as much as 2.5%. Since initiating its payout, the corporate has delivered caffeinated dividend progress. Starbucks has elevated its cost for 14 straight years, rising the payout at a powerful 20% compound annual fee.

Regardless of the seemingly ubiquitous nature of Starbucks shops, the corporate has loads of room to proceed increasing. It at present has greater than 40,000 shops all over the world. Whereas the corporate has in the reduction of on its preliminary plans to open 17,000 new shops by 2030, it nonetheless intends to open many new areas within the coming years.

As well as, the corporate desires to spice up the profitability of its present footprint. That is a part of a broad turnaround effort by new CEO Brian Niccol to get the model again to what it does effectively. These drivers ought to allow the corporate to proceed growing its dividend.

Verizon inventory has declined by about 6% from its current peak, which has helped push its dividend yield to six.2%. The telecom large’s monster payout is on a really agency basis. The corporate generated a gargantuan $19.8 billion in free money stream after capital expenditures final yr. That simply lined the $11.2 billion it paid in dividends. Verizon used the money it retained to strengthen its already rock-solid stability sheet.

Verizon is utilizing its monetary flexibility to purchase Frontier Communications in a $20 billion deal to speed up the enlargement of its fiber community. That deal provides to Verizon’s heavy capital funding in increasing its fiber and 5G networks. These investments ought to develop its money stream, permitting Verizon to proceed growing its dividend. It delivered its 18th consecutive annual dividend improve late final yr, the longest present streak within the U.S. telecom sector.

Inventory market corrections could be nice alternatives to reinforce my dividend earnings. I lately capitalized on the present sell-off by including to my positions in Blackstone, Starbucks, and Verizon. That ought to allow me to earn extra earnings from their larger preliminary yields and better whole return potential as their inventory costs recuperate sooner or later.

Ever really feel such as you missed the boat in shopping for probably the most profitable shares? Then you definitely’ll need to hear this.

On uncommon events, our professional staff of analysts points a “Double Down” inventory advice for corporations that they assume are about to pop. For those who’re frightened you’ve already missed your likelihood to take a position, now could be the most effective time to purchase earlier than it’s too late. And the numbers converse for themselves:

Nvidia:should you invested $1,000 once we doubled down in 2009,you’d have $315,521!*

Apple: should you invested $1,000 once we doubled down in 2008, you’d have $40,476!*

Netflix: should you invested $1,000 once we doubled down in 2004, you’d have $495,070!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable corporations, and there might not be one other likelihood like this anytime quickly.

Matt DiLallo has positions in Blackstone, Starbucks, and Verizon Communications and has the next choices: quick March 2025 $80 places on Starbucks. The Motley Idiot has positions in and recommends Blackstone and Starbucks. The Motley Idiot recommends Verizon Communications. The Motley Idiot has a disclosure coverage.

{kind=link}