Whereas a number of chip shares had convincing performances in 2024, Intel(NASDAQ: INTC) and Superior Micro Gadgets(NASDAQ: AMD) weren’t amongst them. Intel shares fell about 60% final yr, whereas AMD shares have been down about 18%.

Let’s study which semiconductor inventory appears like the higher rebound candidate in 2025.

In a semiconductor market largely being pushed by synthetic intelligence (AI), Intel and AMD have largely been afterthoughts. AMD is the distant No. 2 designer of graphic processing items (GPUs) behind market chief Nvidia. Intel’s market share in GPUs, in the meantime, has dropped to zero, though it wasn’t a far fall, with the corporate having only a 2% market share in PC graphics playing cards in 2023.

AMD has struggled towards Nvidia, largely as a consequence of its inferior software program. In a latest research, SemiAnalysis referred to as AMD’s out-of-the-box GPUs “unusable” for AI coaching, noting it wanted “a number of groups of AMD engineers” to assist it repair software program bugs. Nonetheless, AMD has been capable of carve out a distinct segment in AI inference, with SemiAnalysis saying its prospects usually use AMD’s GPUs for slender, well-defined inference use circumstances.

Nonetheless, AMD has been capable of see robust information middle development, albeit not practically on the identical scale as Nvidia. Final quarter, it noticed its information middle income surge 122% yr over yr and 25% sequentially to $3.5 billion. The corporate credited each its Intuition GPUs and EPYC central processing items (CPUs) for the bounce in gross sales.

CPUs act because the mind of a pc, whereas GPUs have superior processing energy. Whereas there may be a variety of deserved consideration on GPUs, AMD has been doing an excellent bounce within the CPU market, noting that it has been taking share within the CPU server market whereas it additionally has been doing properly within the PC market.

General, AMD noticed its Q3 income climb 18% to $6.8 billion and its adjusted EPS bounce 31% to $0.92. So the corporate has nonetheless been rising properly regardless of the dip in its inventory worth.

Intel, then again, noticed its income decline final quarter by 6% to $13.3 billion, and its adjusted EPS flip to a lack of -$0.46 versus a revenue of $0.41 a yr in the past. The one brilliant spot final quarter was its information middle and AI section, which noticed income rise 9% to $3.3 billion. Nonetheless, when in comparison with Nvidia and AMD, that could be a very modest achieve on this section.

In the meantime, its largest section, Shopper Computing, noticed its income drop 7% to $7.3 billion. By comparability, AMD noticed its Shopper section income surge 29% final quarter to $1.9 billion, displaying it is making some inroads on Intel’s major PC enterprise.

Maybe Intel’s greatest woes, although, stem from its Foundry section, which has been a giant drag on its outcomes. The corporate has poured cash into this enterprise by capital expenditures (capex), constructing out new manufacturing services. Nonetheless, the section has been a persistently giant cash loser, together with reporting a $5.8 billion working loss final quarter, or $2.7 billion when excluding a noncash impairment cost.

Following the exit of its CEO Pat Gelsinger, Intel has stated it may look to spin off its foundry enterprise. The enterprise lately acquired $7.86 billion in direct funding and a 25% funding tax credit score from the federal government to proceed to construct out its manufacturing footprint within the U.S.

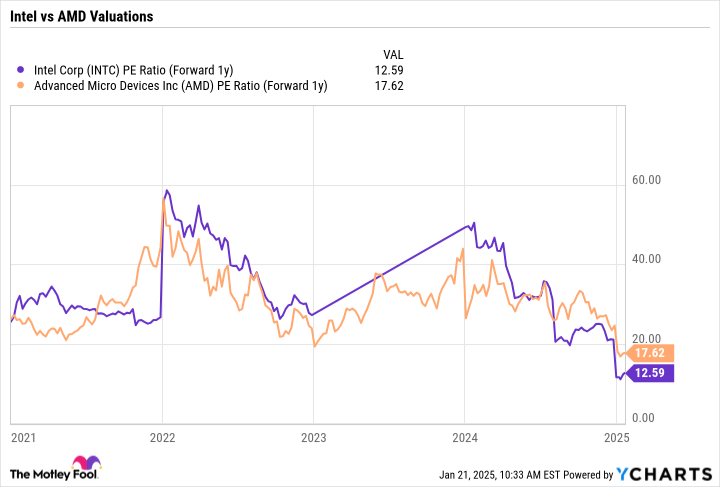

From a valuation perspective, Intel is the cheaper inventory, buying and selling at a ahead price-to-earnings ratio (P/E) of 12.6 occasions versus 17.6 occasions for AMD.

Nonetheless, should you individually worth Intel’s core enterprise and its foundry enterprise, its valuation is much more engaging.

Intel’s foundry enterprise has been shedding a number of cash, nevertheless it additionally has a variety of bodily property. Intel has spent $68.5 billion in capex, totally on the foundry enterprise, for the reason that finish of 2021 and has $104 billion in bodily property on its steadiness sheet. In the event you take simply its latest capex spending and subtract out its $26 billion in web debt, its foundry enterprise could be price about $10 per share on 4.3 billion in shares. It additionally owns an 88% stake in Mobileye, which is price about $11.4 billion, or $2.66 per Intel share.

As such, it’s no shock that the corporate has been the topic of takeover rumors. There are a variety of hidden bodily property not mirrored in its share worth, to not point out the federal government’s direct funding and tax incentive.

AMD, in the meantime, has definitely been the stronger of the 2 companies, though it hasn’t gotten the investor respect it might deserve. If extra AI infrastructure turns towards AI inference, it might be in an excellent place. In the meantime, buyers should not overlook its CPU enterprise, which has been gaining share each in information facilities and PCs.

I like each inventory as turnaround candidates this yr. I like Intel barely extra due to the deep worth I believe remains to be within the inventory. Nonetheless, AMD additionally appears like a stable rebound candidate. Thankfully, buyers haven’t got to decide on and may add each shares to their portfolios in the event that they select.

Ever really feel such as you missed the boat in shopping for essentially the most profitable shares? You then’ll wish to hear this.

On uncommon events, our skilled crew of analysts points a “Double Down” inventory advice for firms that they suppose are about to pop. In the event you’re nervous you’ve already missed your probability to take a position, now’s the most effective time to purchase earlier than it’s too late. And the numbers communicate for themselves:

Nvidia:should you invested $1,000 once we doubled down in 2009,you’d have $381,744!*

Apple: should you invested $1,000 once we doubled down in 2008, you’d have $42,357!*

Netflix: should you invested $1,000 once we doubled down in 2004, you’d have $531,127!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable firms, and there is probably not one other probability like this anytime quickly.

Geoffrey Seiler has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Gadgets, Intel, and Nvidia. The Motley Idiot recommends the next choices: quick February 2025 $27 calls on Intel. The Motley Idiot has a disclosure coverage.

{kind=link}